The recent surge in natural disasters across Massachusetts has highlighted the importance of comprehensive home insurance coverage. While some companies offer competitive rates, others may prioritize profit over customer satisfaction, leaving homeowners vulnerable during times of need. This guide will help you navigate the complexities of the Massachusetts home insurance market and identify the best home insurance companies Massachusetts has to offer.

Toc

- 1. Understanding Home Insurance in Massachusetts

- 2. Factors Affecting Home Insurance Rates in Massachusetts

- 3. Top Home Insurance Companies in Massachusetts

- 4. Protecting Your Home with Specialized Coverage

- 5. Tips for Finding the Best Home Insurance Policy

- 6. Getting a Home Insurance Quote

- 7. Frequently Asked Questions

- 8. Conclusion

Understanding Home Insurance in Massachusetts

Home insurance in Massachusetts is essential for protecting your property against various risks. Here’s a breakdown of key aspects to consider:

Types of Coverage

Home insurance policies typically cover several essential areas, including:

Dwelling Coverage: Dwelling Coverage protects the physical structure of your home. This includes the roof, walls, foundation, and attached structures like garages and decks. It covers damage caused by events like fire, windstorms, hail, vandalism, and theft. However, it typically excludes damage caused by earthquakes or floods.

Personal Property Coverage: Personal property coverage safeguards your belongings inside your home, such as furniture, electronics, clothing, jewelry, and artwork. It covers losses due to the same perils covered by dwelling coverage. You can often choose a separate deductible for personal property, which may be lower than the dwelling deductible.

Liability Coverage: Liability coverage protects you financially if someone is injured on your property or if you accidentally damage someone else’s property. It also covers legal defense costs if you are sued. For example, if a guest trips and falls on your icy sidewalk, liability coverage could help cover their medical expenses and legal fees.

Additional Living Expenses: This coverage helps pay for the costs of living elsewhere if your home becomes uninhabitable due to a covered event.

Policy Types

In Massachusetts, homeowners generally choose between two main policy types:

- HO-3 (Standard Policy): This is the most common type of home insurance. It provides broad coverage for the structure of the home, personal property, and liability.

- HO-6 (Condominium Policy): Designed for condo owners, this policy focuses on the interior of the unit and any upgrades made. The condo association’s master policy typically covers the exterior of the building and common areas.

Factors Affecting Coverage Limits

When selecting a policy, it’s crucial to consider how various factors influence your coverage limits and premiums:

- Home Age and Condition: Older homes or those needing repairs may incur higher insurance costs.

- Location: Homes in flood zones or coastal areas might face increased premiums due to higher risk.

- Replacement Cost: The estimated cost to rebuild your home directly affects your coverage limits. Keep in mind that it may differ from the market value of your home.

- Credit Score: In some states, insurers use credit scores to determine premiums. A higher score could mean lower insurance costs.

Factors Affecting Home Insurance Rates in Massachusetts

Understanding the factors that influence home insurance rates is essential for Massachusetts homeowners. Here are the key elements to consider:

Location

The proximity of your home to coastlines or areas prone to natural disasters significantly impacts your insurance rates. Homes located in high-risk areas, such as those near the ocean or in tornado-prone regions, often face higher premiums due to the increased likelihood of damage from natural events. Insurers take these risks into account when determining coverage costs, making it essential to understand how geography plays a role in your insurance expenses.

Home Age and Condition

The age of your home and its overall condition are crucial factors in determining insurance costs. Older homes may present unique challenges, especially if they require extensive repairs or renovations to meet current safety standards. Additionally, homes built with outdated materials, such as knob-and-tube wiring or lead-based paint, may pose greater risks, leading to higher insurance premiums. However, well-maintained older homes often qualify for discounts because of their craftsmanship, historical significance, and durable building materials that may withstand the test of time better than some modern counterparts.

Home Replacement Cost

The estimated rebuilding cost of your home is a fundamental element in calculating your premiums. Generally, the higher the estimated reconstruction cost, the more you can expect to pay in insurance. Factors such as the quality of construction materials, local labor costs, and regional building codes will influence this estimate. It’s important to work with your insurer to regularly reassess your home’s value and replacement cost to ensure you have adequate coverage without overpaying.

Home Features

Certain features of your home can raise your insurance rates significantly. For instance, having a swimming pool, trampoline, or wood-burning stove may increase your risk profile, leading insurers to charge higher premiums. These items are often associated with a greater likelihood of accidents or liabilities. Additionally, certain home security systems or fire safety features may help mitigate risk and could potentially lower your rates, so it’s worth discussing these aspects with your insurance provider.

Claims History

Your personal claims history, along with the claims history of your neighborhood, can have a profound effect on your insurance rates. Frequent claims can signal a higher risk to insurers, resulting in increased premiums. For example, if your neighborhood has experienced a series of burglaries or severe weather events, your insurance premiums may increase due to the perceived higher risk associated with the area. It can be beneficial to maintain a good claims history and consider preventive measures to minimize risks.

Deductible

Choosing a higher deductible can substantially lower your monthly premiums, but it also means you’ll have to pay more out-of-pocket in the event of a claim. This decision requires careful consideration of your financial situation, as unexpected repairs or damages can create financial strain. Balancing lower premiums with a deductible that you can realistically afford is crucial to ensuring you are adequately protected without jeopardizing your financial stability.

Dog Breeds

Some insurance companies may adjust rates or even exclude coverage for specific dog breeds deemed aggressive. For example, breeds like Rottweilers, Pit Bulls, and Doberman Pinschers may lead to increased premiums or restrictions in coverage. If you own a dog, it’s essential to check with your provider about their specific policies regarding dog breeds, as this can significantly impact your overall insurance costs.

Wind and Hurricane Deductibles

For homeowners in coastal areas, it’s vital to be aware of higher wind and hurricane deductibles, which are often expressed as a percentage of the dwelling coverage limit. These specialized deductibles can significantly affect your out-of-pocket costs in the event of a claim related to storm damage. Understanding these deductibles is essential for homeowners in risk-prone areas, as it may require additional financial planning and preparedness for potential weather-related incidents.

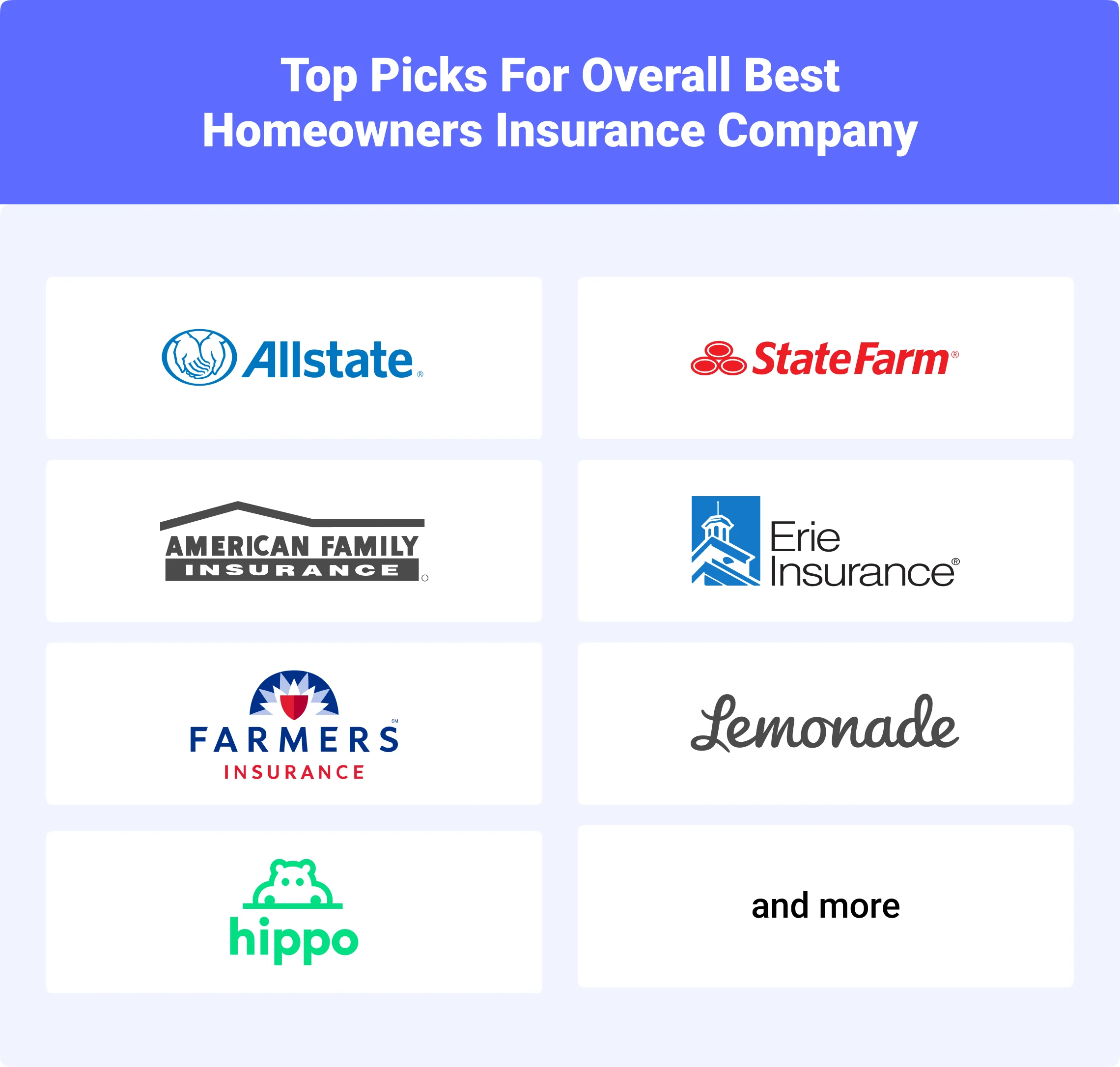

Top Home Insurance Companies in Massachusetts

When searching for the best home insurance companies in Massachusetts, a few providers consistently stand out due to their financial stability, customer service, and comprehensive coverage options.

Amica Mutual is frequently recognized for its excellent customer satisfaction ratings. They offer a wide range of coverage options, including extended replacement cost and identity theft protection, making them a strong contender for homeowners seeking comprehensive coverage.

Another top-rated provider is Chubb, known for providing exceptional coverage for high-value homes. Their policies include increased limits for personal property and liability, ensuring that homeowners can protect their significant investments effectively.

Mapfre Insurance has established a solid reputation in the Northeast, offering competitive rates and a variety of discounts for Massachusetts homeowners. Their regional focus allows them to provide tailored solutions for local residents.

For homeowners seeking personalized insurance solutions, Quincy Mutual Group is a great option. As a local insurer, they are known for their excellent customer service and customized coverage options.

Travelers is a national insurance provider with a strong financial foundation. They offer flexible policy options and a range of discounts, helping homeowners save on their insurance premiums while ensuring adequate coverage.

In addition to these top contenders, other well-regarded regional and national carriers, such as Andover, Arbella, and Plymouth Rock, also serve the Massachusetts home insurance market. Each of these companies offers competitive rates and reliable coverage.

Protecting Your Home with Specialized Coverage

While standard home insurance policies provide essential protection, many Massachusetts homeowners may benefit from specialized coverage options tailored to their unique risks. Here are some options to consider:

Flood Insurance

Given Massachusetts’ vulnerability to flooding, homeowners should consider purchasing separate flood insurance. Standard home insurance policies often exclude flood coverage, so securing a dedicated policy can be crucial for protection.

Umbrella Liability Coverage

For high-net-worth individuals, umbrella liability coverage provides additional protection beyond the limits of standard home and auto policies. This coverage is essential for safeguarding against significant liability claims.

Equipment Breakdown Coverage

This add-on coverage helps cover the costs of repairing or replacing essential home systems and appliances, such as HVAC, plumbing, and electrical systems, in case of mechanical failure. It’s a practical option for homeowners wanting extra peace of mind.

Cyber and Identity Theft Protection

With the rise of cyber threats, homeowners may want to consider cyber and identity theft protection coverage. This specialized insurance helps protect against financial and legal consequences stemming from cyber attacks or identity theft incidents.

Tips for Finding the Best Home Insurance Policy

To help you secure the best home insurance policy, consider the following practical tips:

Get Multiple Quotes

Always compare quotes from at least three to five insurance providers. This essential step not only allows you to find the most competitive rates but also helps you discover various coverage options that are tailored specifically to your unique needs. Each insurer may have different policies and pricing structures, so an extensive comparison ensures that you make an informed decision that best fits your financial situation and protection requirements.

Assess Your Needs

Evaluate your home’s features, location, and personal insurance requirements to determine appropriate coverage limits and deductibles. Take into account factors such as the age of your home, the value of your belongings, and any risks associated with your area, such as natural disasters or crime rates. Understanding your unique situation will empower you to make informed decisions that provide the best protection for your home and assets.

Look for Discounts

Inquire about available discounts with your insurance provider. Many insurers offer savings for bundling policies, installing security systems, or being a loyal customer for an extended period. Additionally, discounts may be available for being a member of certain organizations or completing home safety courses. Don’t hesitate to ask about all potential savings that could lower your premium and enhance your coverage.

Review Policy Details

Before purchasing a policy, thoroughly read and understand the terms, conditions, and exclusions. This step is crucial, as overlooking specific details could lead to misunderstandings down the line. Knowing what is covered and what is not will help you avoid any potential coverage gaps that could leave you vulnerable in case of an incident. Pay close attention to the claims process and any limitations that may apply to your policy.

Work with an Agent

Consider collaborating with a local insurance agent who has expertise in the home insurance market. They can provide personalized guidance tailored to your specific needs and help you navigate the complexities of home insurance in Massachusetts. An experienced agent can also assist in finding the best deals and ensure that you fully understand the coverage options available to you, making the whole process smoother and more efficient.

Getting a Home Insurance Quote

Obtaining a home insurance quote in Massachusetts is a straightforward process. Many insurance companies and comparison websites offer user-friendly online quoting tools, allowing homeowners to receive and compare multiple quotes quickly and easily. Alternatively, you can reach out to local insurance agents who can assist you in finding the right policy tailored to your needs.

Frequently Asked Questions

Q: Is home insurance required in Massachusetts?

A: While home insurance is not legally mandated in Massachusetts, most mortgage lenders require homeowners to maintain a minimum level of coverage as a condition of the loan.

Q: How often should I review my home insurance policy?

A: It’s generally recommended to review your home insurance policy at least annually. This ensures it continues to meet your needs and addresses any changes in your home or lifestyle.

Q: What should I do if I have a claim?

A: If you need to file a home insurance claim in Massachusetts, contact your insurance provider promptly, provide all necessary information, and follow their instructions throughout the claims process.

Conclusion

Finding the best home insurance companies in Massachusetts is essential for protecting your valuable investment against various risks. By understanding the factors that influence home insurance rates, exploring top providers, and following the practical tips outlined in this guide, you can secure the best home insurance policy for your unique needs and budget. Remember to shop around, compare options, and work closely with an insurance agent to ensure your home and assets are adequately protected. With the right coverage in place, you can enjoy peace of mind, knowing that your most significant investment is secure.